Wolfspeed (WOLF) Investment Research Report

Market is pricing in a recovery narrative ahead of fundamentals: AI power electronics and defense demand drive a second growth curve.

Investment Rating

Rating: Buy

Target Price: $80.00

Core Catalysts: AI data center power demand, defense aerospace expansion, SiC industry cycle recovery

Technical View: Strong base formation around $40 with breakout structure forming

1. Investment Summary

Wolfspeed is transitioning from a 'distressed restructuring story' into an AI infrastructure growth beneficiary. While near-term revenue and margins remain weak, market attention is shifting toward 2–3 year growth potential driven by AI data centers, industrial electrification, and defense applications.

As a leading global silicon carbide (SiC) player, Wolfspeed benefits from increasing adoption of high-efficiency power semiconductors in next-generation AI servers and high-voltage systems. Debt restructuring has significantly reduced liquidity risk, allowing investors to refocus on long-term strategic value.

We believe Wolfspeed could experience both earnings recovery and valuation re-rating, with a 12-month target price of $80.

2. Business Overview

Wolfspeed is one of the most vertically integrated silicon carbide companies globally, covering substrate, epitaxy, and device manufacturing.

Its Mohawk Valley 200mm fab represents one of the earliest large-scale 8-inch SiC production lines, providing a strong first-mover advantage in next-generation power semiconductors.

3. AI Data Center Growth Driver

AI infrastructure is becoming a new demand engine for SiC technology. As GPU power consumption increases, data center power architecture is shifting toward higher voltage and higher efficiency systems.

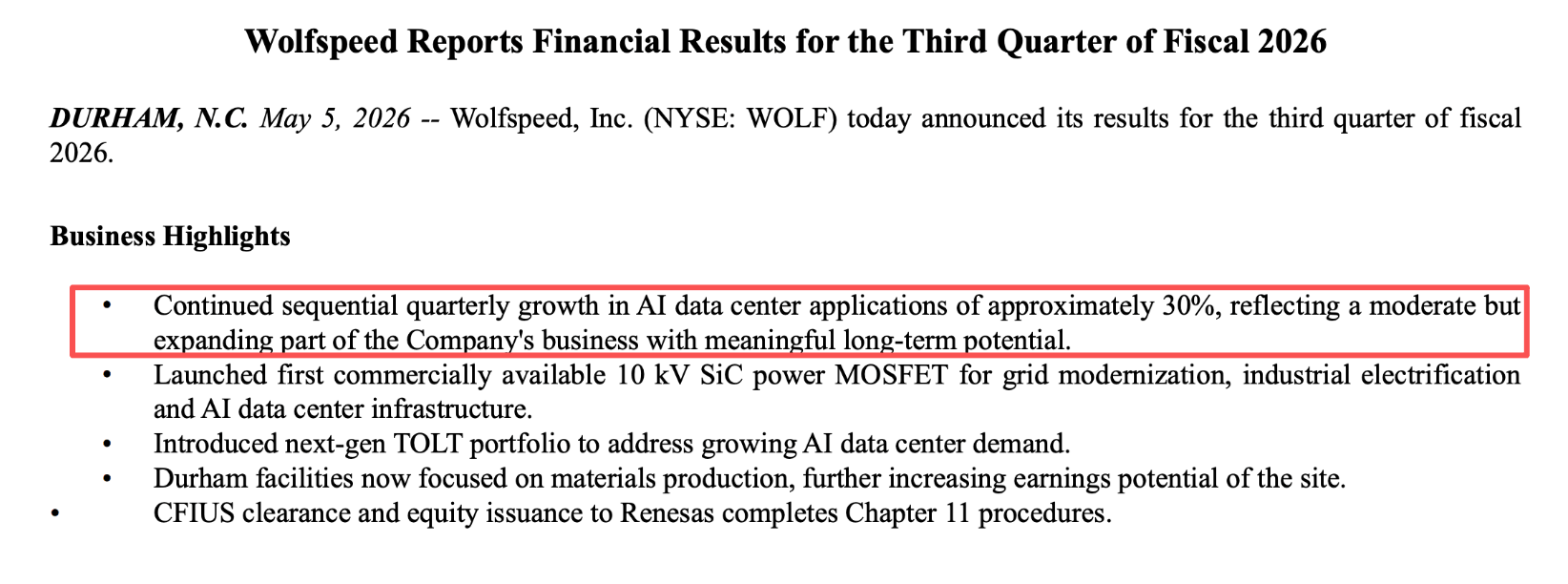

Wolfspeed management disclosed that AI-related revenue is growing approximately 30% quarter-over-quarter, making it the fastest-growing segment of the business.

4. Defense & Aerospace Opportunity

Defense and aerospace applications provide higher-margin, more stable demand for SiC devices, including radar systems, avionics, and missile guidance systems.

5. Valuation Analysis

Current EV is approximately $3.5 billion, implying an EV/S multiple of ~4–5x based on expected revenue recovery.

If AI data center demand and industrial utilization improve, valuation could expand to 6–8x EV/S, supporting a fair value range of $70–80 per share.

6. Technical Analysis

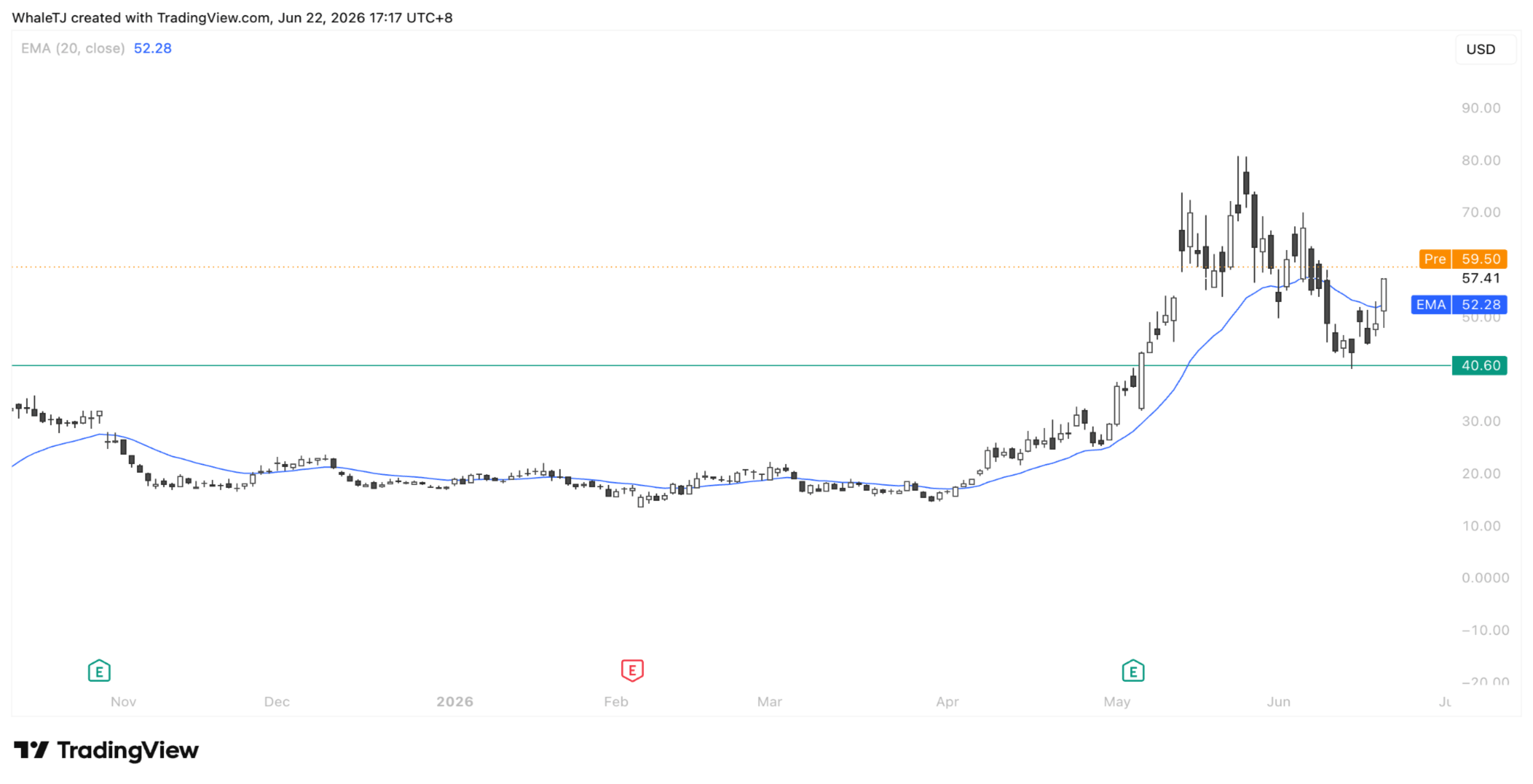

After a sharp correction in June, WOLF found strong support around $40 and rebounded with increasing volume.

Key levels: $40 major support, $52 trend line, $60 breakout resistance, $80 long-term target.

Conclusion

Wolfspeed is undergoing a structural re-rating as AI infrastructure and defense demand reshape the silicon carbide industry outlook. While fundamentals remain in transition, the market is increasingly pricing in a multi-year growth recovery.